Published April 1, 2022

Inflation, Rising Rates & Inventory Challenges - Q1 2022 Real Estate Recap

With spring weather in the air, the real estate market will be seeing its usual uptick, with more homes starting to hit the market and plenty of buyers out there on the hunt for the next place to call their own! As always, there is a ton of talk surrounding home prices and whether they’ll be coming back down, interest rates now that they’re back on the rise, and the never-ending question of if we’re in a housing bubble or not – so we thought this would be a great time to do a deep dive into all of the factors that affect the real estate market to get a true picture of the changes we’ve been experiencing over the last few years and give our take on the million-dollar question of whether or not a crash is coming our way.

1. Home Prices

The National Association of Realtors has been tracking data on home prices since the early ‘70s and how fluctuations in the market relate to the predicted long-term average sales price. We crossed the long-term average line in the early 2000’s when we hit peak home prices in 2005-2007. We all know how that ended and eventually we saw home prices fall back down and they have sat far below the line ever since. That is, until last year when the median sales price finally caught back up to the predicted average. This means that while the spike in home prices from 2019 to 2021 felt like a huge jump, it’s actually a sign that home prices are getting back to what they were expected to be at this time.

2. Inventory

You’ve probably heard people comment on the low inventory of homes on the market, the extremeness of which is illustrated in the graphic above. We can see that since 2013 we have sat steadily below 6 months of inventory. December 2020 and December 2021 experienced the two lowest months of inventory ever recorded at under 2 months, which brought about a velocity of sales that was “unheard of” until we experienced it firsthand.

Comparing today’s numbers to those in ‘05 –’07, we see more good news than bad: if we are using this statistic as an indicator of a market in trouble, we can see that the current trend is a stark contrast to what happened with inventory during the Great Recession when there was a huge uptick of distressed sales. The lack of inventory of course presents its challenges as well since it is a large factor in what propels the hesitation of many sellers to move – understandably, you don’t want to move if you don’t know where you will go. This, however, only further perpetuates the low inventory cycle and makes it a challenge to solve which is why an increase in new construction homes being built, which we’ll go over below, is a huge factor in alleviating the current low-inventory struggle that we’re experiencing.

3. Mortgage Rates

In the 2010’s and early 2020’s, interest rates have remained well under the historical averages of past decades. Many people in the real estate industry have never experienced truly high interest rates, and have been living in what Keller Williams CEO, Gary Keller, has described as, “the cheapest era of money.” It is worth noting that people were still buying homes in the 1980’s when interest rates hit a record high at 16.63%! Comparatively, the recent spike in interest rates back to the 4% mark are really nothing to complain about!

4. Affordability

In terms of affordability, which looks at whether or not the average consumer can qualify for a mortgage loan on a typical home, things did get slightly worse in 2021. Though home prices are not the only thing to blame – inflation overall has caused everything to become more expensive which factors into a borrower’s debt to income ratio and affects their qualification. While we are still looking at below-average affordability overall, first-time home buyers are especially feeling the squeeze. In general, they are experiencing greater barriers to entering the market than ever before. One of the biggest concerns for younger home buyers is student debt, which takes up an average of 24% of a prospective buyers’ income! Because real estate is still one of the best long-term investments, this could hinder these younger generations in the long run since they may be spending more money on rent and other housing alternatives that do not earn them equity over time.

5. Inflation

Inflation is all around us at this point and it’s no secret that it’s at a 40-year high right now, and way above the target rate of 2%. Caused by a shortage of supply brought on by the pandemic, which triggered prices of just about everything to skyrocket, the US government is grappling with ways to stabilize these rates, which are projected to decrease steadily over the next few years. One of the ways to do that is to increase the federal interest rates. We know from history that this is a strategy that has worked before, and in fact has saved us from going into a depression. Because there is a lot of guesswork that goes into adjusting interest rates, there is always the chance that adjusting rates can backfire and overstimulate the economy or ground it, but economists remain optimistic that the market will correct itself.

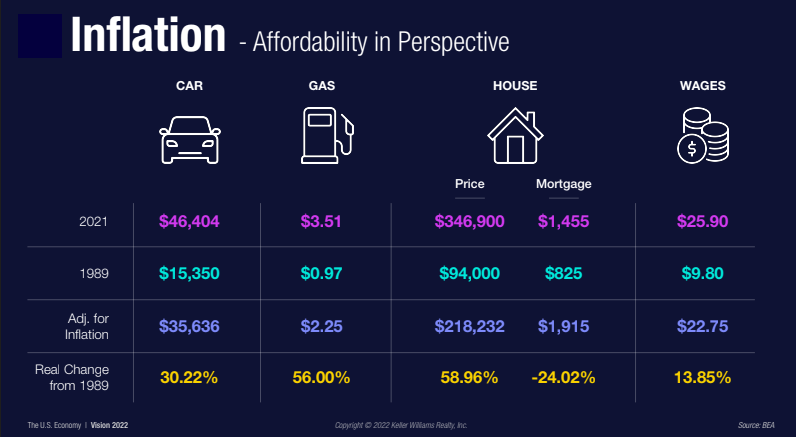

One of the most common things that we’re hearing is that buyers and sellers feel that due to the increase in home prices, that housing in Vermont is no longer affordable or within their reach. While this may feel like the case, it doesn’t necessarily tie directly into the cost of homes themselves - when we compare mortgage costs and the rise that house prices have seen, to the inflation that other goods like gas, cars and wages have experienced, we can see that cost of purchasing a home has actually stayed much more affordable in comparison and the increase in costs of other goods coupled with the lack of adjustment to wages may be more to blame for this.

In the above image, you can see the prices in 2021 vs 1989 as well as adjustment for inflation (the price at which it was projected these things would cost at this point) and then the change in percentage. You can clearly see that while gas prices and home prices themselves have risen by more than 50% more than anticipated due to inflation, because of interest rates and other measures in place to help keep homes more affordable, monthly mortgage payments are actually 24% less than what was expected. This is often why we tell people not to focus so much on the sales price itself, as the monthly payment. Real estate remains to be one of the best investments you can make and borrowing money to do so is generally quite affordable at this time – just think if you’d purchased a house last year in March you’d have paid an average of $359,000 for the home and this March you could have sold it for an average of $457,000 - that’s not a bad return for one year’s time!

What may be more troubling, though, is that while things like cars, gas and house prices have risen dramatically, wages have not kept up with them, leaving many Americans to accumulate increased debts to be able to continue affording the things they need to live which in turn has an effect on what they can qualify to borrow and thus it affects housing affordability as a whole, as we discussed previously.

6. New Construction

The last piece of the puzzle that’s important to consider is the impact and importance of new construction in the market. Why is new construction so important? As we add more new homes to the market, it helps to solve the inventory crisis, which we know in turn helps prices to stabilize. For the past few years, we’ve been underbuilding new homes by about 2.5 million across the United States. In 2008, new home building suffered an enormous stall which we’ve been trying to crawl out of ever since and this lack of new inventory has been a significant contributor to rising home prices.

In 2020 we finally hit the long-term average line! This is great because it means we are adding more new homes to the market than we had been in years, however, we have a lot of lost time to make up for. Catching back up with new construction numbers is one of the most promising ways to be able to steady home prices and help level out our supply and demand issues.

Is this a Bubble?

The big question for many people is: is this a bubble? This is always a worry when home prices spike, since the fear is with prices at record highs, eventually the market will flip and properties will depreciate, leaving people who purchased at these high prices in a negative equity situation. This is what happened during the Great Recession and is a huge topic of conversation since the pandemic first hit. However, the differences between these two situations and time periods are what we believe is the key. Lenders have maintained strict lending requirements, which we know what not the case in 2005-2007, so over time we should not see the defaults and distressed sales we saw in the years following. The start of this situation is also not due to housing – it’s due to the pandemic which changed the way the world thought and operated. The government also seems to have learned a thing or two since that situation and has been much more proactive in trying to maintain a healthy economy.

So the answer is no, we are not in a bubble, not yet at least. If we continue on this steep trajectory as far as home prices and inflation go, we may get to the point where we are in a bubble but for now the differences between now and what we saw in the Great Recession are promising. I do believe that home prices cannot continue rising forever and they will eventually stabilize, however I do not expect them to come down as some buyers seem to be holding out hope for. Most market experts predict home prices will continue to rise another 9-12%. Inventory pressures certainly do not seem like they’re going anywhere and we will continue to have far fewer homes than demand requires which as we know helps keep home prices elevated and the market healthier overall.

As with everything we have to look at the whole picture to get an accurate view of what’s going on - I think many consumers have a slightly skewed view of the market because they only consider one or two factors - if we just look at home prices and nothing else of course it seems like the market is outrageous. If we only look at interest rates from the past three years and not from the past twenty, interest rates rising to 4% again seems like a lot, but when we take the time to analyze how all of the pieces fit together as one, we see a much more accurate assessment of the current market and where we might be headed.

I of course love talking about real estate so if you have any questions, want to discuss the market or are thinking about buying or selling, please reach out!

GET IN TOUCH

|

or another way