Published May 1, 2022

April 2022 Real Estate Market Update

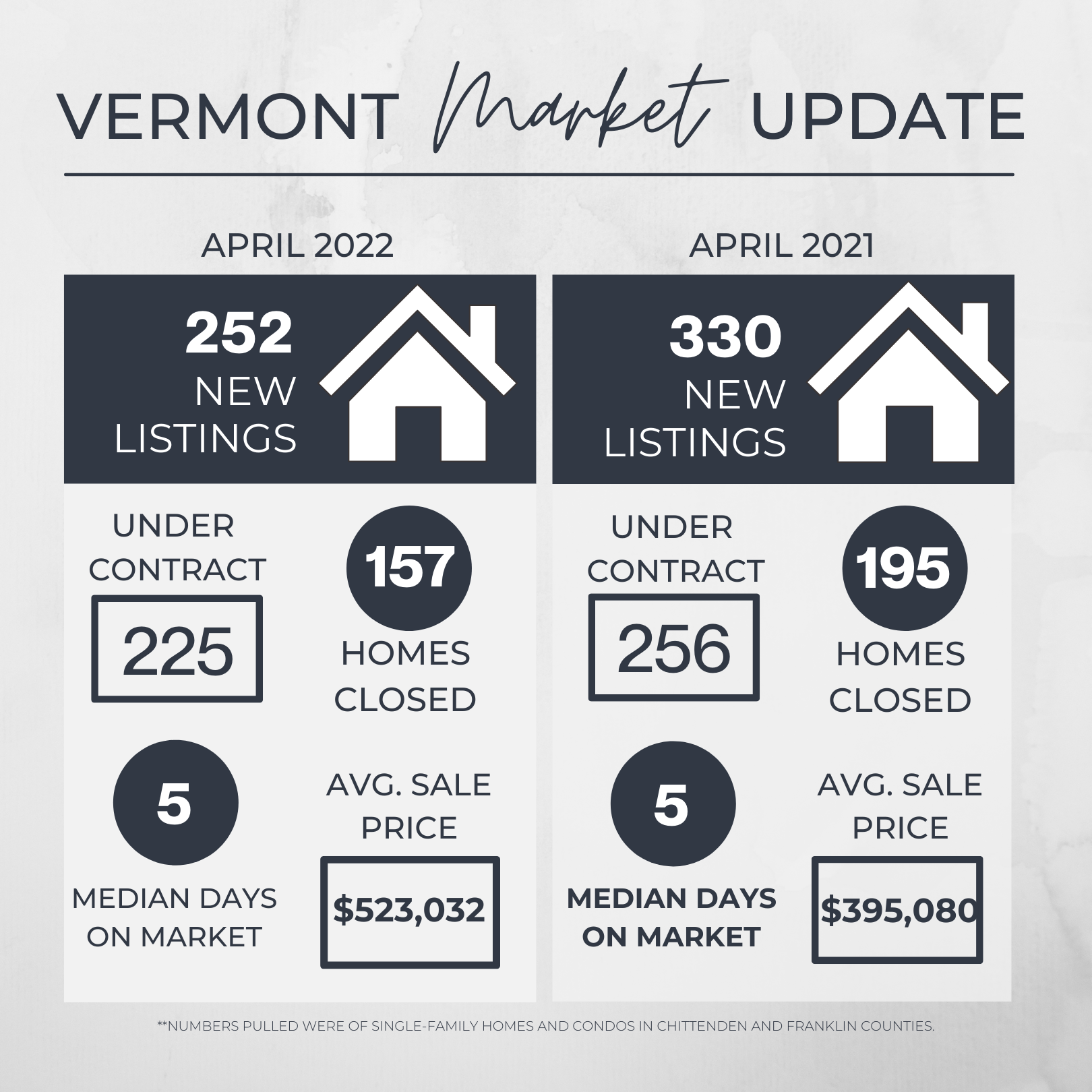

APRIL 2022 REAL ESTATE MARKET UPDATE

Spring weather is in the air, but we're not seeing as much of an uptick as we typically do this time of year in terms of the real estate market. Inventory remains low, with just 1.7 months of unsold inventory nationally, and interest rates are on the rise with the hopes of slowing the ever-increasing home prices, pricing many buyers out of the market and making sellers wary of moving. Yet despite all of this, household wealth sits at record-highs due to equity gained from rising home values and gains from the stock market, even with the recent price declines. So what can we expect to see over the coming months?

Inventory Will Continue to Be One of Our Largest Hurdles

There just aren’t as many homes coming on the market as there are buyers looking to buy. Compared to just last month, we saw a 9% in new listings but when compared to April of last year we saw a drastic dive of over 24% in new homes that hit the market. Understandably, so much of the challenge with selling right now is figuring out where you and your family will move to. That, coupled with the fact that as a homebuyer, having a contingent sale as part of your offer can make it harder to get it accepted, means that many homeowners are deciding it’s not worth the effort and are staying put for a while longer. It’s a tricky challenge to solve really, and the more months we continue to see the number of homes going under contract stay almost the same as the number of new listings that come on the market, the further we perpetuate this cycle that drives increased competition and ultimately leads to higher home prices.

Rising Interest Rates to Slow the Growth of Home Prices

We’ve all been seeing the effects of inflation and soaring prices across all goods. In response to this record-high inflation, the Federal Reserve recently raised mortgage rates in an effort to slow the growth of home prices and cool the market. At the end of March, interest rates topped 5%, and when compared to 2021 where we saw an average rate of 2.96%, the impact this will have on buyers' purchasing power is extreme. Back in December, the average 30-year fixed mortgage rate was 3.11%, which for a $400,000 house would cost you just over $1,700 per month. Contrast that to a rate of 5% which puts that same mortgage at $2,147 per month, adding up to an additional $157,000 dollars over the lifetime of the loan!

And while we’ve already seen some buyers decide to put their home buying dreams on pause, we’ve likely only just begun to see the true effects that these rising rates will have since many buyers that had previously been preapproved had their lender lock them into a lower rate before the rates spiked. So new buyers that enter the market are the ones who will notice the difference with higher monthly payments and lower prequalification amounts. Many buyers will be priced out of market altogether and some may choose to stay put if they can’t afford what they want. Already, banks are seeing a decrease in mortgage applications and new purchase contracts coming in.

The type of buyer that will be most affected by the change in rates will be the first-time buyers that are not reaping the rewards of the equity gained in the form of a home sale like buyers who already own a home are seeing. The segment of home sales where we’re likely to see the most impact will be in the lower price ranges. If you were previously approved for up to $350,000 and now the rates only allow you to qualify for $299,000 or lower, you can see how that would drastically affect the type of home you have to choose from as well as your ability to compete in multiple offer situations.

So What's the Good News?

It’s not all bad news, though. The silver lining is that the rising interest rates should start to bring about some steadying in home prices which is good news for buyers in the long-term. Home prices will not come down by any means, but we should start to see a slowing in the rate at which they continue to rise and with some buyers leaving the market, we may see less competitive multiple offer situations over time. Another awesome thing is, as we mentioned above, we’re seeing record-high household wealth across the country due to the equity gained from the rise in home prices along with elevated returns from investing in the stock market. This is great because buyers have been able to reach into their savings to win multiple offer situations or be able to level up in their price bracket and not put themselves at risk when doing so. Of course, this isn’t going to be possible for everyone, but it’s certainly a good sign when the market is so hot, that people still have money and savings and we’re not largely relying on credit and loosely vetted mortgage loans like we were in 2006.

If you’re currently looking to buy a home, here are three things you can do to reduce the impact of the heightening interest rates and make yourself more likely to succeed on your home buying journey:

Increase your downpayment

One of the best things you can do as a buyer, not only to make your offer stronger but also to reduce your interest rate, is to save up enough money to have a strong downpayment. While you can get a loan with as little as 3.5% down, increasing to 10% or if you’re able 20% is a serious gamechanger.

Offer flexibility

Another thing that really helps your chances of having a successful homebuying experience is flexibility. Knowing that so many sellers are hesitant to sell because they don’t know where to go means its likely you’ll encounter a situation where the seller needs to secure Suitable Housing, in other words, purchase or rent a new home before they sell the current one. So offering flexibility on timing is a huge selling point that likely won’t cost you much in terms of dollars in the long run.

Start your search earlier than you think is necessary

This allows you to not get stuck in a position where you’re feeling rushed or making hasty decisions but it also allows you to be able to offer the flexibility we mentioned above.

For more of our real estate news, tips and advice, reach out to me directly.

Plus, if you're ready to start the search for your perfect home, click here to view all the listings currently for sale.

Or if you have a home to sell? Find out how much you could sell it for here.

Increase your downpayment

Offer flexibility

Start your search earlier than you think is necessary

GET IN TOUCH

|

or another way